Moury Construct ($MOUR)

Missing the obvious

Taking a step away is sometimes the answer to seeing the most obvious opportunities.

A couple of weeks ago I read a write-up in MicroCap Club by @pepersoons (Twitter) about Moury Construct. It looked like an undervalued construction company with some cash in the balance that made it look cheap on a FCF/EV optic.

I might have spent about 3-5 minutes with it. I am not a fan of the low margins and cyclicality of the construction businesses, nor the high capital intensity. I did what I do most of the time, go on to read some other stuff.

On an unrelated note, I have spent the last couple of months doing long walks, trying to give my head some silent time to process all the info that we are exposed to daily. Especially in the stock picking business, the amount of information you need to process is considerable.

So, the week following encountering Moury Construct, for some reason, I kept going back to this name when doing the long walks, but couldn’t figure out why.

I then decided to go back to the article to re-read it. I have to say I have not felt dumber in a while.

This is not any construction company. Moury is a negative working capital business with half of its market cap in cash (€100m out of €200m).

Yes, negative working capital for a construction company. Most of the projects they do are for public entities that pay in advance, so their working capital looks like this:

They are a fourth-generation business in Liège, Belgium, and they have managed to build deep relationships with the public administration, gaining contracts not only to build affordable homes but also to renovate older public European buildings. You can translate this article about the history of the company easily.

They have considerable amounts of European public funding as a tidal wave for their growth.

They are also signaling strong growth for the following year, especially with some new contracts to be announced in September 2024. The fact that they set this fixed date probably means that these contracts will be also public (concessions) thus generating more of a negative working capital situation.

On top of that, they are sitting on a considerable number of ongoing projects, €187m, and backlog, €245m. In FY23, they did €194m in sales and they bought another company for €9m.

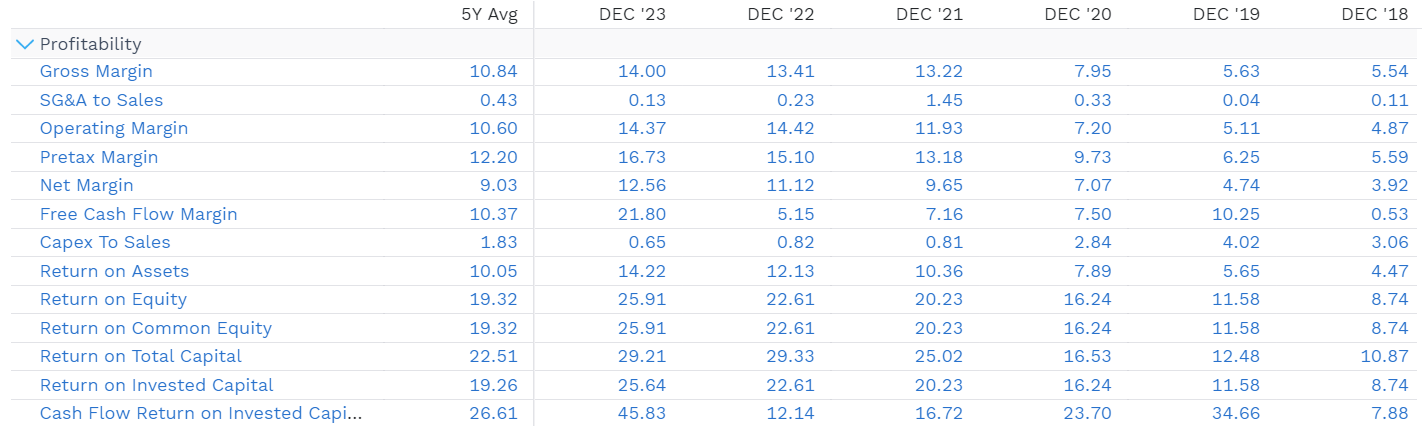

They are generating around 15%-20% of FCF/EV per year. Their return on capital is impressive:

They own some niche businesses doing specialty jobs. You can check their different companies in their annual report.

Something curious and a probable reason for their undervaluation is that they only published their annual statements in French, with no analyst cover. Also, a low transaction volume per day keeps the big ones away.

From 2013 to 2022 they referred to their guidance as looking to the next year “avec sérénité”, which is a beautiful expression (with serenity). My translation is, “Hey, we have a huge cash position and might see some growth, so we couldn’t be calmer about the future”.

In 2022 things changed. They changed their phrasing and directly said that they were expecting a record year in 2023, and that is exactly what happened.

And then 2024 came. I love French so here is a copy paste:

“Le groupe devrait confirmer, d’ici septembre 2024, la signature d’un nombre important de nouvelles commandes. Nous anticipons donc un niveau d’activité robuste pour les prochaines années.”

They are signing more (I assume public) contracts in September, so they are anticipating robust activity for the next years.

Neither growth nor cheapness is what brings my attention to this company. When you are operating a negative working capital (self-funding operations) and have half of your market cap in cash, there are very few things that can go wrong. Cheapness (15%-20% FCF/EV) is an extra for this high-quality company. And growth might be a catalyst.

Shares are illiquid so I have had to buy for a couple of weeks. The share price has gone from €535, when I read the article, to €635 now. I don’t move that much volume so clearly, some people have already discovered the opportunity.

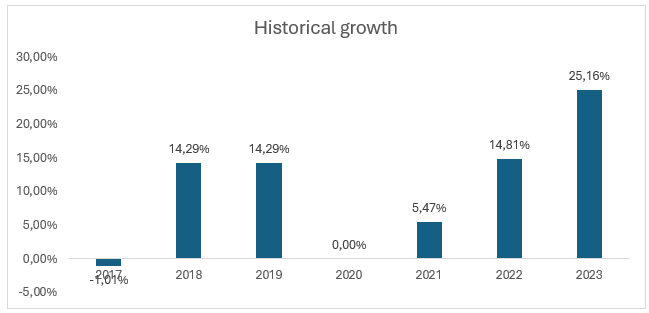

Growth in their latest years:

Expectations:

With these kinds of numbers and the balance sheet that the company has, I see two things:

• An antifragile position at a cheap price

• An easy path to +20% IRR if some cash is given back to shareholders, which they stated, is in their plans.

Companies like this are not a “bet half your portfolio in it”, but rather a derisked and easy way to make above average results. If I could find enough of these “simple plays”, my entire portfolio would consist of them, with some small exceptions to provide optionality.

What I like about companies like this is the certainty and predictability of cash flows. Public construction/renovation is funded on a multiyear horizon by the EU.

I do not have the stomach to build big positions in more speculative ideas, so using the barbell approach is what works for me. Taking decent positions (I am doing around 9%) in these kinds of ideas, and smaller ones in things with optionality (thinking about Moberg) is the way I do it.

I own other similar businesses (in my opinion), like BELFB or CZBS where the outcome is very predictable and there is a non-complicated path to >15%-20% IRR for some years.

But here is the thing. If it's simple for me it is also simple for the rest of the market so you need to take action quickly when these little opportunities exist.

My unwillingness to pay a bit more for a package of shares has turned the above yields in green from the 20s to the 10s while I waited for the stock to drop, which never happened.

I prefer my portfolio to be like a Toyota rather than a Tesla because the path to wealth is muddy, arduous, and long. Let's go for resilience.

Simple is beautiful.

Simple is reliable.

I hope they initiate a buyback or some (safe) bolt-on acquisition (not too big) to get the cashpile working. I am not too happy with using the cash to invest in the stock market, that is not their job, but ours.

I saw some concerns about more private contracting work in the mix, but that does not bother me too much. The government can also be a pain and the local Walloon government is very unstable in terms of debt and deficits. Not saying that they will not pay the bills, but they may reduce investment and real estate projects. The private business can pick up the slack.

High quality name in any event with an ironclad reputation in the market.

Thanks for highlighting this company. I also immediately dismissed it in the past after 3-5 mins.

After your post here, I stumbled on this report from the AGM (in dutch): https://www.vfb.be/artikel/verslag-van-de-av-bij-moury-construct

Here are some highlights (my own translation):

Q: Will you put the net cash to work?

A: We're conservative. Construction is a cyclical, we have survived previous dips with our strategy

The cash is "put to work". Up to 25% is invested in the stock market: ETFs & stocks, 50% of that in commodities (one is named: Barrick Gold). Also holds some reserves in physical gold.

The cash buffer gives customers confidence.

Q: Recent (small) acquisition was partially financed with issued shares. Why?

A: The sellers wanted to receive part of the price in shares.

Q: Why not use the shares on your balance sheet?

A: Wasn't really answered. MOUR holds 4584 shares or 1.14% shares, almost €3m

Q: What's the plan with the shares you bought back?

A: No plans yet, they will stay on the balance sheet.

Q: Why not pay more cash as dividend?

A: Dividend has been growing, and we'd like 10% yearly growth... but will stay prudent. Depends on yearly results.

Q: Why are you so much better (4x better ROIC) than comps like CFEB.BR? Cyclical peak?

A: Lower overhead, high quality work => no litigation, stability & loyalty from employees.